Weekly Reports

Weekly Market Report

In the United States, the sector-specific Purchasing Managers’ Indexes (PMIs)—which serve as leading indicators of economic activity—for March came in above 50 points. It is important to note that this threshold separates economic expansion from contraction. In this environment, yields on U.S. Treasury bonds rose across most maturities, with the exception of the 1-year bond, which edged down slightly to 3.74%, while the 10-year bond yield rose to 4.43%. This week, attention will focus on March labor market data, with projections of 60,000 new jobs created and an unemployment rate of 4.4%, while developments regarding the conflict in the Middle East are awaited. Given that inflationary risks are persistent, interest rates are expected to remain high by historical standards, even though the central bank anticipates another rate cut (currently at 3.75%) later this year. In this environment, it seems prudent to secure higher nominal yields today compared to those that might be available later for investment-grade bonds, with a focus on positions with maturities of up to 5 years.

Weekly Monitor

International

The focus this week in the United States will be on March employment data, with projections of 60,000 new jobs created and an unemployment rate of 4.4%. Additionally, February retail sales figures—a proxy indicator of economic activity—will be released, while on the geopolitical front, a resolution to the conflict in the Middle East is awaited. In the Eurozone, preliminary March inflation figures will be released, with estimates pointing to a year-over-year increase of +2.7% and +2.3% for the measure excluding food and energy (core), while in the United Kingdom, the final fourth-quarter Gross Domestic Product (GDP) data will be published, with expectations of +1.0% year-over-year growth.

In the United States, preliminary data for the March sectoral Purchasing Managers’ Indexes (PMIs) came in above 50 points, the threshold separating expansion from contraction in activity. Thus, the manufacturing sector registered 52.4 points, the services sector 51.1, and the composite index 51.4 points.

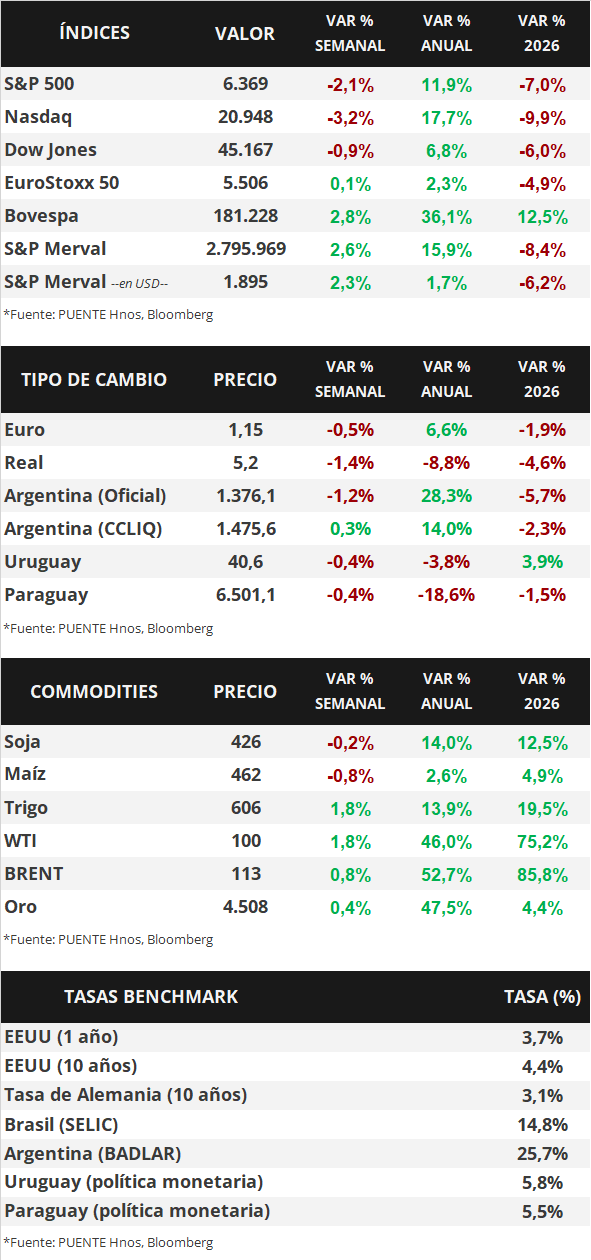

In this environment, U.S. Treasury yields rose across most maturities, with the exception of the 1-year note, which fell from 3.79% to 3.74%. Meanwhile, the 3-year yield rose from 3.90% to 3.93%, and the 10-year yield from 4.38% to 4.43%. Investment-grade corporate bonds (LQD ETF) closed with a yield of 5.7%. As for the major U.S. stock indices, they traded lower, with the Dow Jones posting the smallest decline (-0.9% for the week).

In Latin America, the Central Bank of Chile kept its monetary policy rate unchanged at 4.5%, in line with expectations. In contrast, in Mexico, the central bank opted for a quarter-point cut to 6.75%, contrary to the consensus expectation among analysts that the rate would remain unchanged. Against this backdrop, the Chilean peso weakened by 1.1%, while the Mexican peso strengthened by 1.2% for the week.

Weekly Market Report

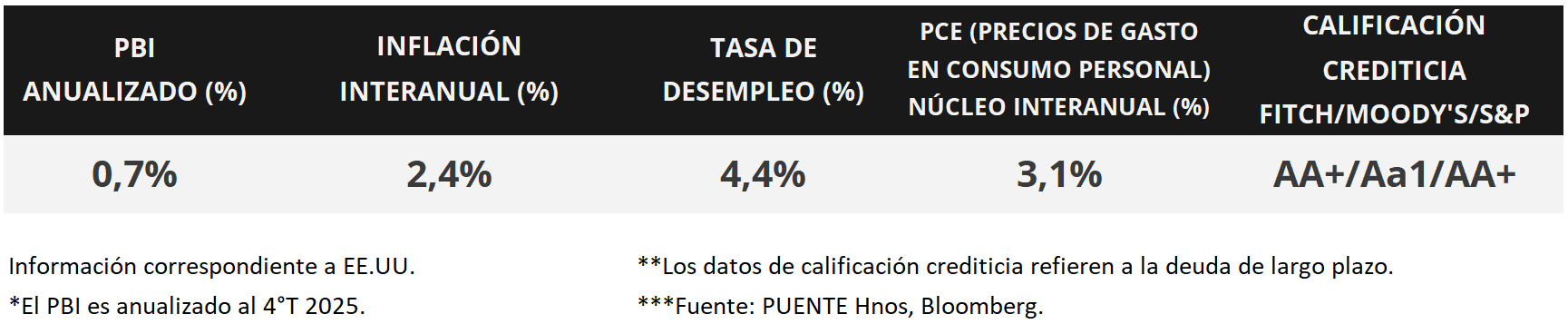

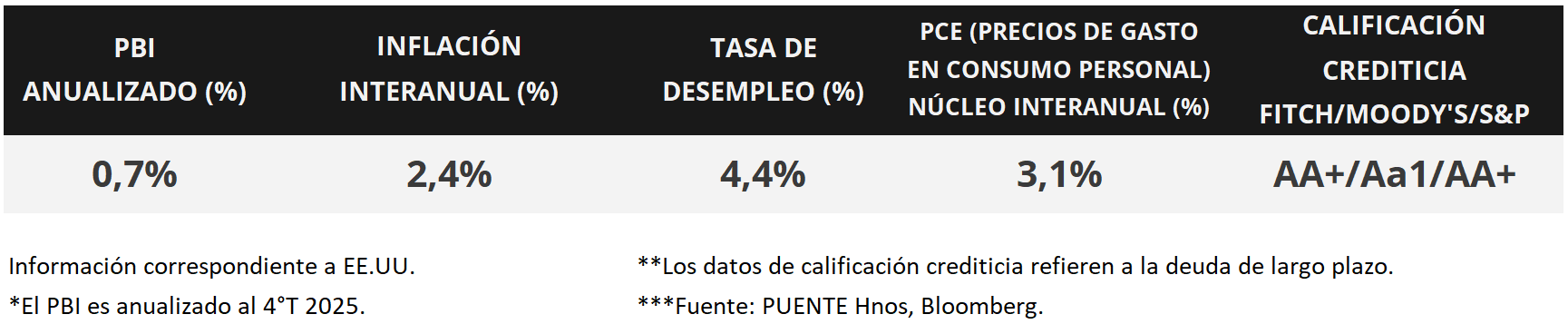

The U.S. Federal Reserve (Fed) kept the federal funds rate unchanged at 3.50%–3.75%, in line with expectations. Regarding monetary policy, it maintains its projection for a quarter-point cut this year, which would bring the benchmark rate to a range of 3.25%–3.50%. In terms of outlook, for 2026 the Fed improved its growth projection (+2.4%) and PCE inflation forecast (which measures household personal consumption expenditures and is the Fed’s preferred indicator for monetary policy decisions: +2.7% annually for the core measure excluding food and energy), while maintaining its unemployment projection (4.4%). In this environment, U.S. Treasury yields continued to widen across the entire curve, with the 1-year bond at 3.79% and the 10-year bond at 4.38%. This week, attention will remain on the geopolitical front as the outcome of the conflict in the Middle East is awaited; meanwhile, the March sectoral Purchasing Managers’ Indexes (PMIs) will be released. With persistent inflationary risks, interest rates are expected to remain high by historical standards, making it prudent to secure higher nominal yields today compared to what might be available later for investment-grade bonds, with a favorable strategy being to position in maturities of up to 5 years. In other news, the European Central Bank kept its policy rate at 2.15%, in line with expectations.

Weekly Monitor

International

The focus in the United States this week will remain on geopolitical developments, as the world awaits updates on the conflict in the Middle East. Meanwhile, preliminary March data for the sector-specific Purchasing Managers’ Indexes (PMIs) in the United States and the Eurozone will be released. In Latin America, the central banks of Chile and Mexico will hold monetary policy meetings; their benchmark rates currently stand at 4.5% and 7.0%, respectively.

The Fed kept the benchmark rate unchanged in the current range of 3.50%–3.75%, in line with expectations. The decision is based on a labor market with low job creation and an unemployment rate that has changed little in recent months, alongside a still-high inflation rate. In this regard, the Fed confirmed that it will continue to monitor data developments to balance the risks to its dual mandate: price stability and full employment. At the same time, it highlighted the uncertainty surrounding the economic outlook due to the conflict in the Middle East.

In the quarterly update of macroeconomic projections, the inflation forecast for 2026 was raised: both the overall PCE and the measure excluding food and energy (core) are expected to be +2.7% year-over-year, versus the previous +2.4% and +2.5% in each case. Growth projections were also revised slightly upward to +2.4% annually, with unemployment remaining at 4.4%. Regarding monetary policy, expectations remain for a quarter-point rate cut this year, which would bring the rate to a range of 3.25%–3.50%.

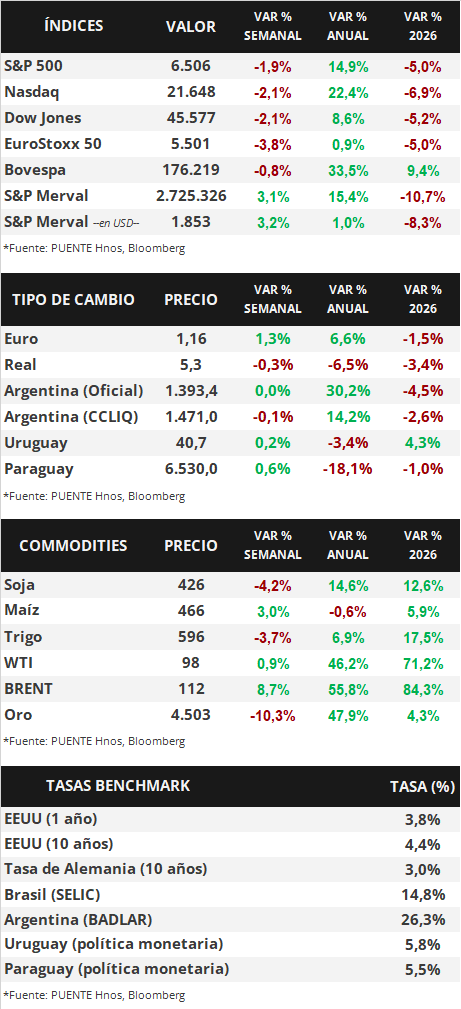

In this environment, U.S. Treasury yields continued to widen across the entire curve during the week, with the 1-year note rising from 3.63% to 3.79%, the 3-year note from 3.74% to 3.90%, and the 10-year note from 4.28% to 4.38%. Meanwhile, investment-grade corporate bonds (LQD ETF) ended the week with a return of 5.5%. Meanwhile, the major U.S. stock indices fell by an average of -2.0%.

In Europe, the European Central Bank kept its policy rate unchanged at 2.15% for the sixth consecutive time. The bank emphasized that it is prepared to act if necessary, considering a potential increase in the cost of financing to mitigate the war’s impact on inflation trends. In terms of macroeconomic outlook, it revised inflation upward for this year to +2.6% annually and +2.3% for core inflation (compared to December estimates of +1.9% and +2.2%, respectively). Meanwhile, more moderate growth of +0.9% is expected, compared to the previous +1.2%. In this context, the euro rose +1.3% for the week to 1.16 euros per dollar.

Likewise, this trend was also mirrored by the Bank of England and the Bank of Japan, which decided to keep their interest rates at current levels of 3.75% and 0.75%, respectively, in line with projections. In both cases, the concern lies in the impact of the conflict in the Middle East on short-term inflation levels.

In Latin America, the Central Bank of Brazil bucked the global trend by cutting the interest rate by a quarter of a percentage point to 14.75%, after six months at 15%, in a more cautious decision than analysts had anticipated. The central bank believes that inflation trends have improved, although the international outlook appears uncertain. As a result, the real fell 0.3% for the week to 5.31 reais per dollar.